2014 China PV Market Record

Abstract Wang Bohua, Secretary General of China Photovoltaic Industry Association, revealed at the seminar "Photovoltaic Industry Development and Investment Analysis - 2014 Review and 2015 Outlook" held recently, facing overseas &ldq...

Wang Bohua, Secretary General of China Photovoltaic Industry Association, revealed at the seminar “Photovoltaic Industry Development and Investment Analysis – 2014 Review and 2015 Outlook†held recently that in the face of the “double reverse†of overseas, China's polysilicon in 2014 The output still reached 132,000 tons, up 57% year-on-year; wafer production reached 38GW, up 28% year-on-year; cell sheet production reached 33GW, up 32% year-on-year; module production reached 35GW, up 27.2% year-on-year. In addition, more importantly, our photovoltaic companies are profitable. "The gross profit margin of the backbone enterprises has mostly returned to double digits, and the business operation has been significantly improved. Enterprises in all links of the industry chain have entered the top ten in the world, such as 4 polysilicon, 8 silicon wafers, 5-6 solar cells, and components. 5-6, and the first place is a Chinese company." Wang Bohua said.

Below, let us look at what is the situation of China's PV market in 2014?

First, the polysilicon link

The number of production enterprises reached more than 18, the production scale increased by 57.1%; the industrial capacity utilization rate increased significantly, reaching 84.6%; the industry concentration was higher, the top ten production accounted for 91%, and the top five accounted for 77%. Product competitiveness has been continuously enhanced and it has already achieved the basis of import substitution.

Second, the silicon link

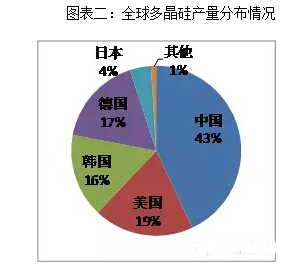

In 2014, China's wafer production reached 38GW, a year-on-year increase of 28%. The production of silicon wafers reached nearly 8.8 billion pieces, accounting for 76% of the world; the industrial concentration is high, the output of the top ten enterprises accounts for 77%, and the top five accounts for 58%; the overall capacity utilization rate of the industry is above 72%. The capacity utilization rate of ten enterprises is above 85%; polycrystalline is still the mainstream, and the ratio of polycrystalline to single crystal is about 83:17.

Third, the battery segment

In 2014, China's battery production reached 33GW, an increase of 32%. The output of the top ten enterprises accounted for 52%, and the industrial concentration needs to be further improved; the overall capacity utilization rate of the industry is slightly lower than 70%, but the capacity utilization rate of the top ten enterprises is above 85%; the proportion of polycrystalline and monocrystalline cells is Around 87:13.

Fourth, the component link

In 2014, China's component production reached 35GW, a year-on-year increase of 27.2%. The output of the top ten enterprises accounted for 56%, and the industrial concentration needs to be further improved; the overall capacity utilization rate of the component industry is lower, but the capacity utilization rate of the top ten enterprises is nearly 90%; the proportion of polycrystalline and monocrystalline cells is 88:12. about.

Fifth, the power station link

In 2014, China's photovoltaic grid-connected installed capacity was around 10.5GW. Due to the policy connection between scale control and the decentralization of the approval authority for photovoltaic power plants, some provinces and cities have issued slower plans, resulting in the centralized construction of photovoltaic power plants at the end of 2014. By the end of 2014, China's cumulative PV installed capacity was 26.52 GW, of which distributed photovoltaic power generation did not exceed 5 GW. China's PV market is still dominated by large-scale ground power stations. Due to the large number of projects that have not been put into operation at the end of 2014 (estimated to be more than 5GW), and some regions have been completed but not included in the scale, it is expected that China's PV market will see a large growth in 2015.

6. Import and export situation

From the perspective of import and export, the import and export situation of China's photovoltaic products has maintained a steady growth and the development trend is good. In 2014, exports of wafers, cells, modules and inverters reached US$15.6 billion, while imports of polysilicon exceeded US$2 billion and imports were close to 100,000 tons.

In 2014, China's component export regions were more diversified, exports to Japan continued to increase, exports to Europe and the United States slowed down, and emerging countries need to be accelerated. Among them, the component exports to Japan accounted for nearly 40%, while the current Japanese market slowdown, the industry will face fluctuations, should be alert to the industry.

Seven, technical level

From the perspective of photovoltaic technology level, the polysilicon link, the liquefied bed method will be mass-produced, such as Shaanxi Tianhong and the US REC joint venture, Jiangsu Zhongneng independent research and development; silicon wafer, diamond wire cutting has been applied on a large scale Monocrystalline silicon wafers and polycrystalline silicon wafer cutting have also been applied on a small scale; battery links, multiple printing, PERC technology, black silicon technology, etc. are already in use or under development.

As the market picks up, the capacity utilization rate of China's PV companies has been effectively improved, the profitability is getting better, and the industry's gross profit margin has rebounded significantly.

The backbone enterprises have high shipments and full production, and some enterprises have a capacity utilization rate of over 85% and a gross profit margin of over 20%.

Chart 13: The trend of gross profit margin of key enterprises in 2010-2014

IX. Problems in China's PV industry in 2014

1. The domestic market environment needs to be improved

First, the record-scale management model needs to be further improved; second, the distributed business model needs to be broken; third, the photovoltaic power station digests the stored pressure, and some areas have abandoned light, and the light rejection rate in some areas has reached more than 20%.

2. Uncertainty in foreign markets

First, there are trade barriers in some export markets, such as the United States and the European Union; second, the development of the sectoral market is weak, such as Japan; third, the development potential of emerging markets needs to be further explored.

3. Technology development has a long way to go

The homogeneity of products is relatively high. There are still some gaps in the research and development of batteries and new batteries in some universities. High-end equipment still relies on imports, such as equipment required for PERC battery technology.

4. Standard testing and certification system needs to be improved

With the increasing attention of the capital market to photovoltaic power plants, the quality of photovoltaic power plants has received more attention. It is urgent to improve the standard certification testing system, and to ensure product quality problems by introducing third-party insurance and urging suppliers to improve service quality.

5, business management still has pressure

The situation of “incremental increase without profit†is still continuing. The rapid increase in supply and market uncertainty will still bring pressure on product prices. Coupled with the “negative†attitude of financial institutions to manufacturing industry, the operating pressure of PV companies in China remains to be determined. Further improvement.

X. Global market outlook

According to the Energy Outlook released by the International Energy Agency on October 7, the cumulative installed capacity of photovoltaics will reach 4,600 GW by 2050, and photovoltaic power generation will account for 16% of the world. To achieve this goal, the annual installed capacity will increase from 36GW at the end of 2013 to 123GW in 2030, and the peak installed capacity of 200GW will occur between 2030-2040.

General Secretary Xi Jinping proposed: "China plans to reach a peak in carbon dioxide emissions around 2030 and will strive to reach an early peak. It is planned to increase the proportion of non-fossil energy in primary energy consumption to around 20% by 2030." By the end of 2014, China's non-fossils Energy accounts for 11.1%. To achieve the 20% target by 2030, PV needs to play a bigger role.

Future crystalline silicon component manufacturing will be mainly located in mainland China, Taiwan, Malaysia and the United States; the cost of mainland China is still the most competitive.

XI. Prospects for industrial development in 2015

Uncompetitive capacity to accelerate the launch - standard conditions for the photovoltaic manufacturing industry

Industry concentration will be further enhanced - PV merger and reorganization

Financial institutions promote the survival of the fittest - financial self-help, financial leasing, securitization

Technological progress is accelerating - more than 18% polycrystalline, more than 20% single crystal

Product quality is getting more and more attention - the need for asset securitization

Distributed generation mode accelerates innovation - capital sought after

Energy storage will grow faster in the new energy sector

Photovoltaic applications accelerate integration

Acid Soldering Flux Paste,Soldering Paste Flux,Solder Flux Paste,Flux Soldering Paste

NINGBO XIHAN TIN SOLDER CO.,LTD. , https://www.soldertop.com